In early May, TRENDFOCUS released various quarterly reports, which reviews the HDD and SSD industries’ performance in CQ1 ’15, and what effect it has on the updated quarterly forecast.

Hard Disk Drives (HDDs) saw a sharp decline to 125M units sold, mainly due to the softness in the notebook PC market. Performance Enterprise Hard Disk Drives were flat, while Nearline Hard Disk Drives fell 5% Q-Q. This is a result of inventory carry over from the record shipments seen in CQ4 ’14.

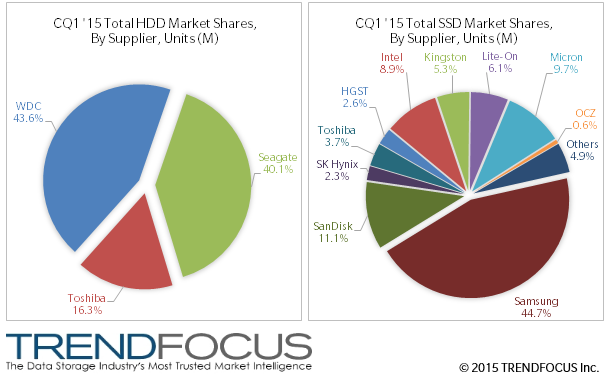

In the SSD market, client SSDs actually increased in sales from CQ4 ’14 by 3.5% Q-Q. Although Drive Form Factor (DFF) type devices saw a decline of 5.1% Q-Q, module type devices saw a healthy increase, 22.4% Q-Q, due to demand in the low end notebook market segment.

Enterprise SSDs saw a decline of 14.2% (Q-Q) mainly due to softness in the enterprise SATA SSD segment with Hyperscale customers. This downturn was a function of record shipments of SATA SSDs in CQ4 ’14, which caused inventory carryover into CQ1 ’15. “We are starting to see some seasonality trends for enterprise SSDs as we have seen with enterprise HDDs in certain segments over the past couple of years,” says Mark Geenen, President of TRENDFOCUS, “Datacenter build-outs are following a certain pattern as it relates to their storage requirements, whether it is for HDDs or SSDs.”

SAS SSDs continue to show good growth, with various Storage Networking companies staying with SAS SSDs for their storage deployments. As it relates to PCIe, it has yet to find its place in the various market segments, whether it be System vendors, Hyperscale, or the Channel. With that said, one PCIe vendor was able to see a major gain in share in the PCIe segment from CQ4 ’14 to CQ1 ’15.